How can we get consumers to try alternative wine packaging?

By Jakob Mesidis, Bill Page, Larry Lockshin, Armando Maria Corsi and Justin Cohen

Ehrenberg-Bass Institute for Marketing Science, University of South Australia

Calls from consumers, advocacy groups, and governments have seen industries adopt practices to reduce their CO₂ output. To this end, the wine industry has done great work in the vineyard and winery—improving soil and fertiliser management, using more carbon-efficient machinery, and finding alternative power sources. But all this doesn’t address the largest area of carbon emissions from wine production: making and moving conventional glass wine bottles (Abbott et al. 2016).

The production and transport of glass wine bottles contributes around 68% of the wine industry’s total CO₂ output (Abbott et al. 2016). Glass bottles are much heavier than other types of packaging and require considerable energy to produce, making the bottle production process a significant source of CO₂ —about 1.25 kg of CO₂ per bottle (Amienyo, Camilleri & Azapagic 2014; Ferrara, Zigarelli & De Feo 2020). They also don’t stack well: a truck or ship full of wine bottles is carrying a lot of air, so more shipments are needed to transport less wine than if the wine was in a more spatially efficient package. And, because glass is heavy, these shipments are consuming even more fuel than they would with a lighter load. All these shipments and all this fuel means more CO₂ emissions. As these carbon emissions are tied back to one process, the wine industry is in a unique position to reduce carbon emissions significantly by making a single packaging change.

Winemakers can use a variety of different packages to reduce their emissions. Casks, cans, and even polyethylene terephthalate (PET) bottles are just some of the pack formats available, each generally being about 40-50% more carbon efficient than their glass counterparts (Abbott et al. 2016; Amienyo, Camilleri & Azapagic 2014; Detzel & Mönckert 2009; Roux & Gérand 2014). However, winemakers quite rightly fear consumer rejection of such packaging. Conventional glass bottles have had a few hundred years to work themselves into the habits and buying repertoires of consumers across the globe. This is a daunting prospect for any winemaker interested in using alternative wine packaging in their product portfolio, but so far there has been no research to help guide those in industry. What will consumers accept? How do the different formats compare? What messages could be used to convince consumers to try something different? While understandable, this hesitancy to move away from glass bottles has ultimately slowed the industry’s progress towards carbon neutrality.

My colleagues and I at the Ehrenberg-Bass Institute at the University of South Australia School of Business, and the University of Adelaide, are working to address this hesitancy by giving winemakers the insights they need to be able to confidently pursue an alternative packaging strategy. We are focusing on one simple question: how do we get consumers to trial alternative wine packages? As with screw caps, we suspect that consumers will adopt alternative wine packaging for at least some of their purchases after trying them.

Simulated shopping

We conducted a discrete choice experiment where we put “shoppers” through a simulated shopping experience, asking them to choose realistic wines from a virtual shelf. In such a choice experiment, “shoppers” are forced to make trade-offs between competing alternatives, and these alternatives are carefully designed to reveal what drives shoppers’ decision making (e.g. ‘is the pack format more important than the brand?’). In our experiment, respondents were informed that they were buying 1.5L of Shiraz for an informal gathering at their home, and were then presented with a series of ‘choice sets’ (see figure 1) and asked to indicate which wine product they would buy.

Figure 1: A choice set used in the experiment.

We included five different variables that we identified as being important in either motivating choice of these alternative packages or changing the way people react to buying: brand, price, message content, message appeal, and obviously, the packaging style itself. We also collected socio-demographic information on respondents—such as age, gender, product involvement, and level of environmental concern—to see whether the effects of these variables differ by consumer type. Finally, to give a bit more context to exactly why people were picking certain packages, we also collected some data on the potential motivators behind people’s preferences for the packaging formats we included.

This research is ongoing, but here in this article we share some preliminary results. These preliminary results come from the soft-launch data of the main survey, with 179 Australian wine buyers (who had purchased wine in the past three months). It’s important to note that this sample was analysed as a single aggregated group. When the full analysis is conducted, segments may emerge that are more reactive to some variables than others.

Packaging format

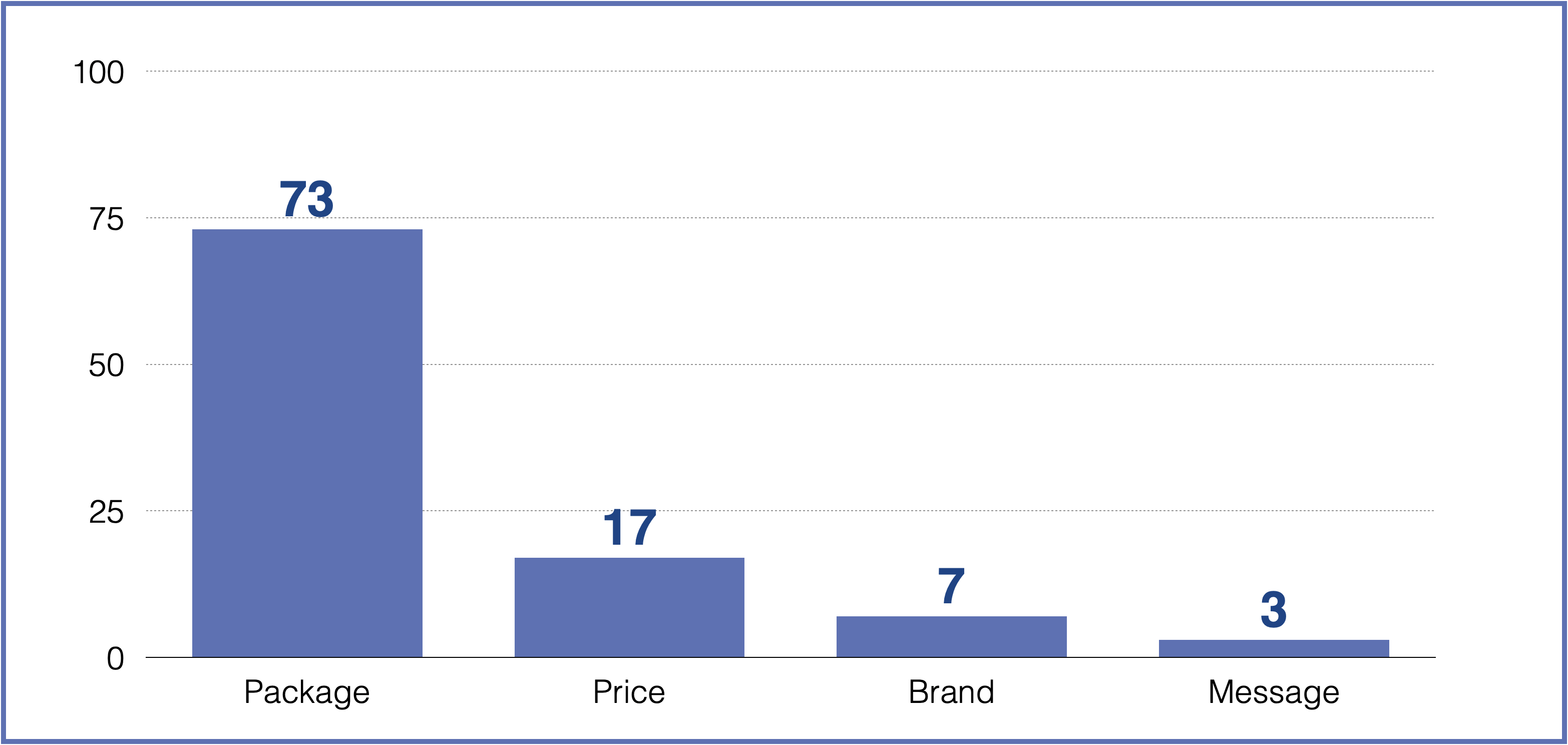

Figure 2 illustrates how important each variable was for respondents (as a percent of all “influence”) when making a wine purchasing decision. Clearly, of the variables that were tested, packaging format was the most important. This was due to the strength of the preference for glass wine bottles. Unsurprisingly, glass was the most preferred format by a significant amount. One of the more atypical packaging formats tested was the flat PET bottle. Interestingly, this package type slightly outscored bag-in-box (anticipated as being the second most popular due to it being well-established in the Australian market) in preference. This may be due to its visual similarity to the conventional glass bottle, aligning more closely with what consumers expect a bottle of wine to look like when compared to the alternatives—or it could be a result of the early stage of analysis, and the results will change as the full data set is analysed. Either way, this holds early promise for the viability of alternative formats in market (although they are all still quite a way away from closely competiting with the dominant preference for glass). Despite their growth in market over the past few years, cans were the least preferred packaging format.

Figure 2: % Importance of each variable in buyer choice

The second most important variable was price. Consumers typically stuck to the middle-low price tiers of wine, which is in line with what we already know about wine buying behaviour —consumers don’t want to break the bank by buying the most expensive option, but also view price as an important quality indicator, so don’t want to risk buying a bad wine.

The third most important variable was brand. The main observation here was a size effect—wines presented with larger and more prestigious brands were generally chosen more often. This has implications particularly for larger wineries, as these results would indicate that alternative packaging strategies are more likely to succeed when attached to a larger brand than they would for smaller competitors.

The least effective attribute was an environmental message. The messages were presented as shelf labels for each of the alternative packaging options, and focused on either the recyclability or low-carbon qualities of each package. Consistent with previous research, consumers responded best to the messages about recyclability. Additionally, they were also more likely to buy when the messages provided specific and detailed information (e.g. 46% more recyclable than standard glass wine bottles, helping reduce landfill), as opposed to more vague and abstract messages (e.g. this package will help build a more recyclable wine industry). In all instances, however, having a message of any type proved to be more effective in motivating trial than no message at all.

So, what does this all mean for wine producers interested in using alternative wine packages? From these results, there is potential for alternative packages, but glass is still king (and is by a longshot). This potential could be best harnessed by bigger wineries, who price these products in the mid to low price tier and emphasise their recyclability benefits in a specific, detailed way. This is not to say that these are the only variables that may have an effect—retail displays, advertising, or region-wide adoption could all play a role, but this research provides a starting point for producers where there was previously none. As the analysis is extended to the rest of the sample, more and more questions can be answered, namely around how these effects vary by consumer characteristics and whether there are any particular segments of note (e.g., a group of consumers that are more highly involved, and prefer more expensive wines attached to more prestigious brands). All this and more to come early 2022, so watch this space!

References

Abbott, T, Longbottom, M, Wilkes, E & Johnson, D 2016, ‘AWRI: Assessing the environmental credentials of Australian wine’, Wine & Viticulture Journal, vol. 31, no. 1, pp. 35-37.

Amienyo, D, Camilleri, C & Azapagic, A 2014, ‘Environmental impacts of consumption of Australian red wine in the UK’, Journal of Cleaner Production, vol. 72, pp. 110-119.

Detzel, A & Mönckert, J 2009, ‘Environmental evaluation of aluminium cans for beverages in the German context’, The International Journal of Life Cycle Assessment, vol. 14, no. 1, 21 February, pp. 70-79.

Ferrara, C, Zigarelli, V & De Feo, G 2020, ‘Attitudes of a sample of consumers towards more sustainable wine packaging alternatives’, Journal of Cleaner Production, vol. 271, 20 October, p. 122581.

Roux, P & Gérand, Y 2014, Comparative Life Cycle Assessment of the NOVINPAK® PET/RPET bottle and traditional glass bottle including vine growing and vine making, Iresta Elsa Group

Co-author Jakob Mesidis was a speaker at the 2021 PACKWINE Forum & Expo

By 2021 PACKWINE Speaker Jakob Mesidis

While we all know that over time alternative wine packaging will play a vital role in the wine industry’s future, do consumers share our enthusiasm and do they have preferences for specific packaging types? Jakob’s presentation will take a look at what packaging types, what kinds of messages and how brand and price contribute to motivating consumer trial of alternative wine packaging. In doing so, we also briefly consider how many and what types of consumers are most likely to trial these packages.

About co-author Jakob Mesidis

As a marketing scientist at the Ehrenberg-Bass Institute for Marketing Science, Jakob likes to approach wine marketing through the lens of the consumer. Jakob’s current area of research focuses on how to best motivate consumer trial of low-carbon wine packaging. Innately curious about all things wine, with an unwavering desire to help motivate progress within the wine industry, Jakob seeks to answer the questions that will lead to the industry’s growth—especially among younger consumers.